While people who contract COVID-19 (Coronavirus) who are under the age of 80 and do not have any pre-existing conditions – such as cardiovascular disease, diabetes, chronic respiratory disease, hypertension or cancer – are most likely to experience only flu-like symptoms, those who are over 80 years’ of age or individuals with pre-existing conditions are certainly at a much greater risk.

To prepare yourself – and your family – for possible infection of the virus, there are a few important first steps to follow:

STEP 1 – Should you experience a combination of the following symptoms, it is important to record these and also to note when these symptoms first began: fever, sore throat, dry cough or breathing difficulties.

STEP 2 – The next important step is to call your local doctor or GP to explain the symptoms and to request advice about the best way to proceed. It is not recommended that you go into the doctor’s consulting rooms because, if you do have the virus, it is vital that the virus does not spread to any of the staff or other patients in the doctor’s waiting room.

Local doctors will be prepared for the call and they will provide very clear guidelines about how to proceed in terms of the testing procedures.

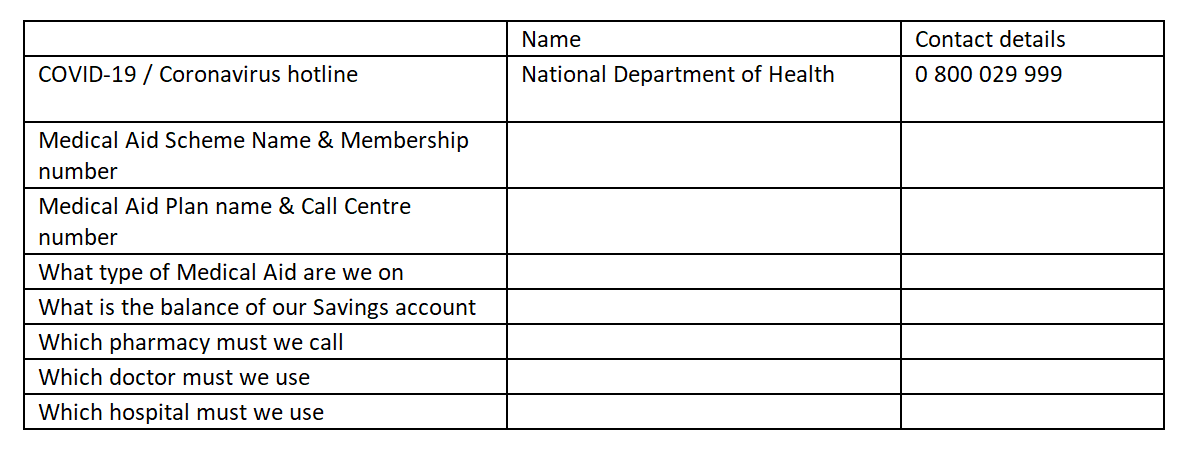

If you don’t have a doctor you can call, there is a National Department of Health Coronavirus Hotline number (080 002 9999) or people can also contact the National Institute for Communicable Diseases (NCID) on 082 883 9920 for testing purposes.

These hotlines were established for concerned citizens and have been specifically set up to deal with the outbreak.

Most medical aid plans have stipulated different cover depending on whether you have tested positive for COVID-19 or negative for the virus.

Even though some medical aids have confirmed that they will cover ‘Out-of-Hospital’ costs related to medical aid members who have tested positive for COVID-19, if your test result is negative, most medical aids have confirmed that you will need to rely on the existing benefits of your selected plan, to bear the costs of testing and diagnosis.

Dr Sipho Kabana, Chief Executive and Registrar at the Council for Medical Schemes, in his recent Press Release (3 of 2020: Medical Schemes and the coronavirus) has confirmed that, as the regulator, they are committed to ensuring that there is effective coverage for members who suffer from – including complications – the coronavirus. “We encourage medical schemes to provide comprehensive cover for all confirmed cases, in the interest of public health,” concluded Dr Kabane.

“As the virus progresses, it may result in various complications, such as pneumonia and respiratory failure, which then should be treated as Prescribed Minimum Benefit (PMB) level of care,” said Dr Kabane. In cases of uncomplicated infection (thus even if you have tested positive), where there are no PMB-eligible conditions, the medical scheme may fund all health care costs as per the scheme rules.

If you are not positive when tested for the COVID-19 virus and – based upon Dr Kabane’s explanation, even if you are positive, without any complications – your consultations, tests and medicine could be handled by your existing medical aid, as follows:

- Entry level plans, which usually have Network doctors available for consultation and provide formulary medication for condition treatment – your diagnosis will likely be covered by your medical aid.

- Hospital plans, which usually do not cater for ‘Out-of-Hospital’ treatment – the cost of diagnosis and testing will be for your own account.

- Saver plans usually provide an allocated Savings amount for ‘Out-of-Hospital’ treatment for the year, to cover consultation and testing. – If this savings account has not already been exhausted, you should have your testing costs covered from your savings account. If your savings allocation has already been exhausted, then you will be responsible for the costs incurred.

- Comprehensive plans usually cater for ‘Out of Hospital’ diagnoses and treatment via, firstly a savings account, and secondly from an ‘Above Threshold Benefit’ account. These two funding accounts are separated by a ‘Self Payment Gap’ which comes into effect once the savings allocation is exhausted, and before a member can enter the ‘Above Threshold Benefit’ account. Payment depends on where you are on the continuum of funding. If you are either in the Savings account or already in the Above Threshold Benefit account your testing costs are likely to be funded by your medical aid. If, however, you find yourself within the ‘Self Payment Gap’, you will be responsible for the costs yourself.

- Traditional Plans usually provide a prescribed benefit for GP visits and another benefit for medication. – If these benefits have not already been exhausted, your diagnosis and testing costs should be covered by your medical aid.

The main medical aid member to share all information with every family member regarding the specific medical aid plan they belong to, so that if the main member falls ill or is unavailable, everyone knows the plan type and what extent of cover they can expect in the event of infection.

Know how your medical aid will treat you if your test positive for COVID-19. Many medical aids have released additional benefits to all their members, providing assurances and confirming that additional ‘Out of Hospital’ benefits will be available for testing, diagnosis and treatment. As I already outlined, it’s also very important to know how your medical aid will handle your bills if you test negative for COVID-19.

Other important must-knows include:

- Know and list your medical aid name, plan type (e.g. Hospital plan, Saver plan etc), your membership number and call center telephone number. This may be required for pre-authorisation or additional information regarding Networks, hospitals, ambulance services, doctors, pharmacies or medicines etc.

- Know how your ‘Out-of-Hospital’ benefits will be provided. Does your medical aid have a savings account, for example? What is the balance in the account?

- Know if your medical aid restricts doctor visits to specific Networks of doctors, or even to a specifically listed family doctor. Make sure that your family is aware of the doctor’s name and contact telephone number.

- Know how prescribed medicines will be paid from your scheme, especially if you are on a Hospital-only scheme, or if your savings account balance is zero.

- Know if your scheme allows for the purchase of ‘Over-the-Counter’ medication from the pharmacy, and if so, make sure you know whether there are any restrictions. Some medical aids limit this benefit to a Rand-value maximum, whilst others provide the benefit up to the balance of the savings account, or even up to a Rand sub-limit.

Getting the right care and attention if you have the Coronavirus is essential. Don’t let a lack of information prevent you or your family members from getting the medical assistance that is needed as quickly as possible. We always advise that individuals should regularly sit with a professional healthcare consultant to navigate some of the more difficult areas within their medical aid plans as this can help the entire family, in the long run.

Below is a useful memo which can be cut out and put on the fridge (especially if you are the one that gets sick), so that everyone will know who to call and what to do.

I have the following symptoms:

Medical Aid useful details:

Medical Aid useful details:

Jill Larkan is the Head of Healthcare Consulting at GTC.